Saving money is very much like putting a seed in the ground and nurturing it. If you are in need of shade right away, you would probably opt for a small umbrella. However, if you desire a majestic tree that can shelter you in the distant future, you will have to wait for years. Similarly, when it comes to money, we refer to these types of decisions as Short Term and Long Term plans.

Each one of us in India has dreams that are very different from one another’s. For example, while a youngster may be looking forward to getting a new bike next year, a parent may be planning to raise funds for the child’s college education. It may be that the grandparent, on the other hand, is looking forward to a serene life after retirement. To achieve these dreams, you must follow the proper route.

Here’s how to choose between short term and long term plans.

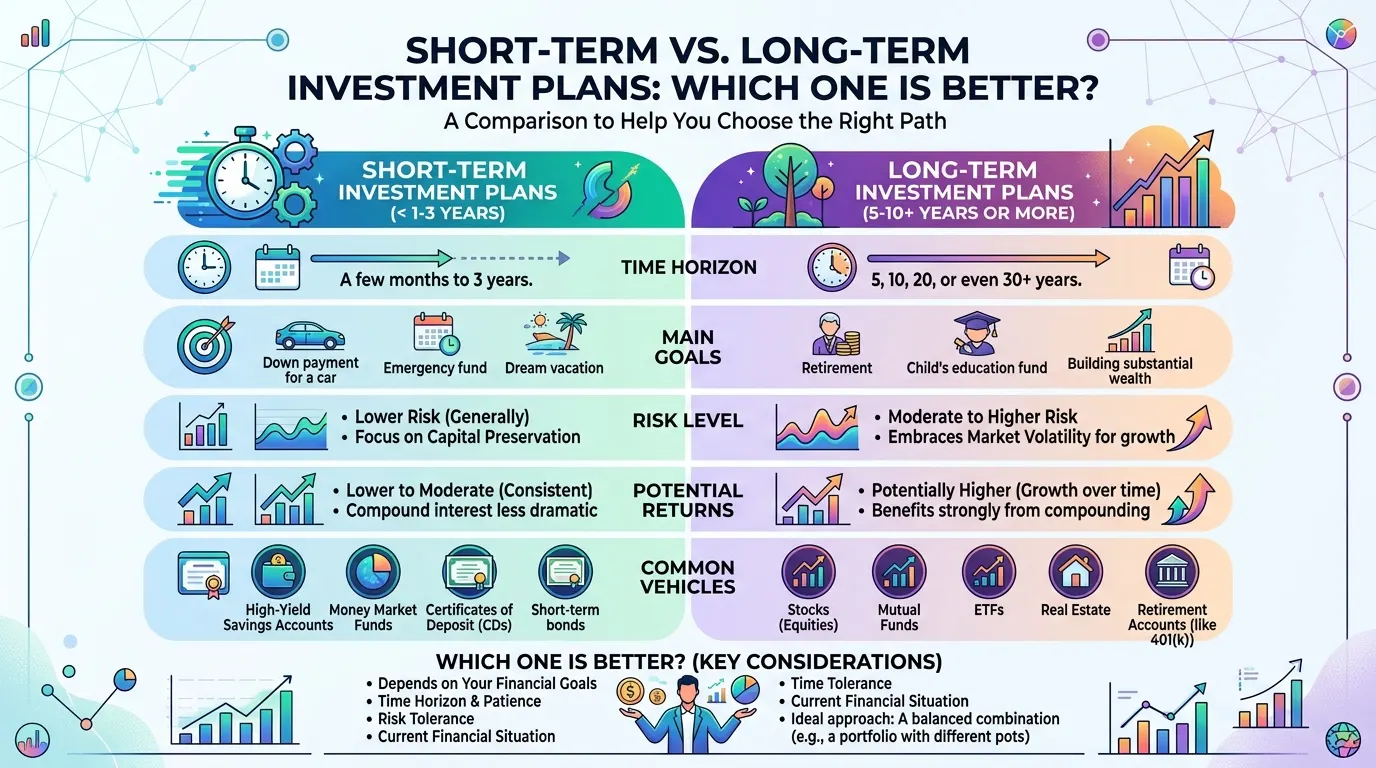

What is a Short Term Investment Plan?

If you have targets that are quick to come to fruition, then short-term investing is for you. Usually, one to three years is the time frame for a short term investment plan. These schemes work like a safe deposit vault; when you deposit the money, it is kept secure. And when you require the funds, you can unseal them pretty fast.

Reasons to opt for short-term:

- Security: The value of your money barely swings.

- Quick Withdrawal: You can have your money in your hands within a few days or even hours.

- Small Targets: Perfect for vacations, phone purchases, or having some backup money.

India examples: Bank Fixed Deposits (FDs), Recurring Deposits (RDs), or Liquid Mutual Funds.

What is a Long Term Investment Plan?

A long term plan is for big dreams. These are goals that are 5, 10, or even 20 years away. Here, you give your money time to grow. In India, things like gold, land, and stocks are popular for the long term.

Why choose long-term?

- Big money: Over several years, small amounts of cash will become large amounts of money. That is the power of “compounding.”

- Rise in prices always: We all know prices of milk and petrol keep going up year after year. By choosing long-term, your funds will grow at a faster pace than these prices.

- Great plans: A long term plan can be your stepping stone to a dream house, a child’s wedding, or your retirement.

The Best of Both Worlds: The ULIP Policy

Sometimes, people want a plan that meets two needs simultaneously. They want to save money and, at the same time, protect their family. To start with, let us tell you what a ULIP policy is.

ULIP is an abbreviation for Unit Linked Insurance Plan. It is a unique plan in India. When you pay for a ULIP policy, a part of your money is used for life cover while the rest goes into investments.

- Life Cover: It provides you with life insurance. When the unthinkable happens to you, your family is given a certain amount of money.

- Investment: The remaining portion of your funds is used to make investments with a view to increasing the amount.

ULIPs are often a good choice if you’re thinking about the long term. The policy binding period (“lock-in” time) is 5 years; that generally means that one should not utilize the money withdrawn before 5 years. Besides motivating one to save tax, it perhaps will also assist the one in staying with a plan!

By managing your wealth in this manner and taking care of your family’s needs under one comprehensive plan is not only a smart thing to do but also one Indian families do, which is the main reason for their popularity with many of them.

Which One Should You Choose?

It is a common misconception that one has to go with only one. Extremely wealthy Indian families do use both. In fact, it is all about achieving the right balance. Let’s consider your money as a cricket team; just as some players are required to score fast, some are needed to remain at the crease for a longer time. Being emotionally attached to one form of saving may expose you to the risk of a sudden expense, but by diversifying your savings, you are ensuring both.

Use Short Term Plans if:

- Time: You must have the money in less than 3 years.

- Safety: You can’t risk this money at all since you will need every single rupee very soon.

- Purpose: You wish to create an “Emergency Fund” for the unexpected, cover annual school fees, or get a new gadget. Such plans keep your money available and on hand for you.

Use Long Term Plans if:

- Time: You can let 5 years or more pass, keeping your money invested without interfering in it.

- Growth: You are looking to accumulate a large amount of money for the most important moments of your life.

- Patience: You don’t mind market fluctuations for bigger rewards later. Normally, such variations in the market tend to normalize over time, and in fact, you’re likely to end up with significantly more than you initially invested. This approach demands a lot of discipline, and it’s definitely the most reliable method of achieving steady growth in your wealth.

Conclusion

Different plans suit different people, and there is no one-size-fits-all plan. The right plan is that which helps you achieve your goal. A long term plan is a good option if you are young. Even a small amount like ₹1,000 a month can be a huge amount over 20 years. If you are closer to retirement, then you should keep more money in short term plans so that you can use it whenever you want.

Start with listing your goals. When you know the time, picking between a short-term and a long-term investment plan becomes very easy for you. Good luck with your investing!