Most conversations about money focus on numbers. Budgets. Interest rates. Credit scores. Spreadsheets. But if you look closely at your bank statement, you will see something else entirely. You will see a record of your moods.

That spontaneous online order after a stressful meeting. The takeout splurge after a long week. The celebratory shopping trip after good news. Spending is not always about need. It is often about emotion. And if emotional spending goes unchecked, it can eventually lead to bigger financial challenges that require solutions like debt settlement just to regain balance.

Instead of asking only, “Can I afford this?” it may be more useful to ask, “What am I feeling right now?” Recognizing your emotional spending triggers is less about self control and more about emotional awareness. When you understand what drives your purchases, you gain leverage over them.

Your Wallet as a Mood Diary

Think of your spending history as a diary written in transactions. Each purchase tells a story. A story about stress, boredom, celebration, or even loneliness.

Emotional spending happens when you use money to regulate feelings instead of addressing the root cause. According to research summarized by the American Psychological Association on stress and coping, people often turn to quick reward behaviors during high stress periods. Shopping offers immediate gratification. It provides a sense of control and a small burst of pleasure.

The problem is that the relief is temporary. The item arrives. The excitement fades. The stress remains. Then you are left with both the original emotion and a lighter bank account.

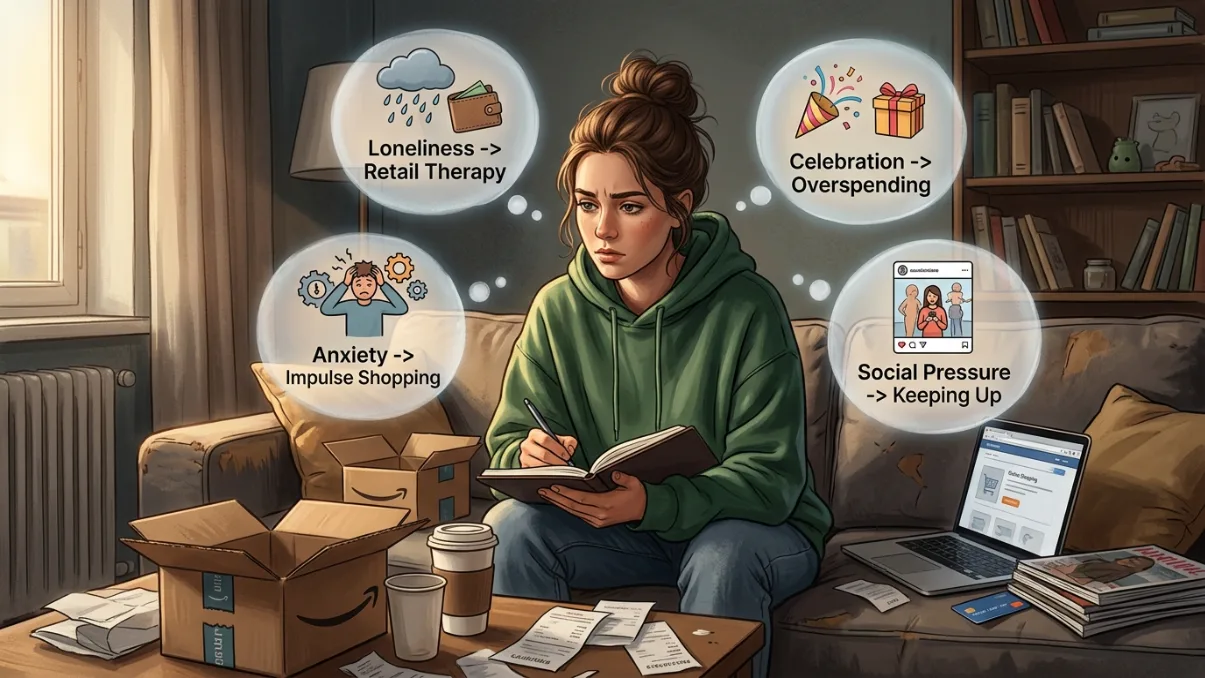

When you review your spending, look for patterns. Do you spend more at the end of exhausting days? After arguments? During weekends when you feel unstructured? Those patterns are clues.

How to Argue in English Professionally (Keeping Relationships)

Boredom Is a Powerful Trigger

Boredom does not always feel dramatic, but it can be surprisingly influential. Scrolling through shopping apps or wandering through stores can feel like something to do. A small purchase adds novelty to an otherwise dull moment.

The brain responds to novelty with dopamine, the chemical linked to pleasure and reward. The Cleveland Clinic explains how dopamine plays a role in motivation and reward cycles, reinforcing behaviors that feel good in the moment. Buying something new activates that system.

If boredom is your trigger, the solution is not necessarily stricter budgeting. It may be more engaging routines. Hobbies. Social plans. Exercise. Learning something new. When your time is filled with meaningful activity, the urge to manufacture excitement through spending often decreases.

Stress Spending Feels Logical at First

Stress spending can be especially tricky because it often feels justified. You tell yourself you deserve a treat. You have had a hard week. You need something to look forward to.

There is nothing wrong with occasional treats. The issue arises when spending becomes your primary coping mechanism. If every stressful event leads to a purchase, the habit strengthens.

The Consumer Financial Protection Bureau offers guidance on managing financial stress, emphasizing awareness and small action steps. Applying that same mindset to emotional spending means pausing before you act. Ask yourself what would actually reduce the stress. Is it a conversation. A walk. A plan to tackle the problem directly.

Often, addressing the source of stress is more effective than temporarily distracting yourself from it.

Loneliness and the Illusion of Connection

Shopping can create a brief sense of connection. You interact with a salesperson. You read reviews. You imagine how a new item will fit into your life. For a moment, it feels engaging.

But purchases cannot replace genuine connection. If loneliness is driving your spending, adding items to your cart will not fill that gap for long.

Recognizing this trigger requires honesty. If you notice that you shop more when you feel isolated, focus on building real connection instead. Reach out to a friend. Join a group. Volunteer. The emotional return on those investments is far greater than any product.

Celebration Spending Can Also Spiral

Emotional spending is not always negative. Positive emotions can trigger it too. You get a bonus. You finish a project. You feel proud. Spending becomes a way to amplify the moment.

Celebration is healthy. Rewarding yourself can reinforce progress. The key is intentionality. Decide in advance how you will celebrate milestones. Set a reasonable budget. Align the reward with your values.

Without boundaries, celebratory spending can quietly undermine financial goals. The goal is to enjoy success without erasing it.

Creating a Pause Between Feeling and Purchase

One of the most effective strategies for managing emotional spending is creating space. A simple pause can interrupt the impulse.

Try a twenty four hour rule for non essential purchases. Add items to a wish list instead of your cart. Notice how often the urge fades once the emotion passes.

You can also name the feeling directly. Saying, “I am stressed,” or “I am bored,” reduces the intensity. It shifts you from reacting to observing.

Over time, this awareness builds a new habit. Instead of automatically spending when emotions spike, you check in with yourself first.

Replacing the Reward Loop

Since emotional spending often involves a dopamine reward cycle, it helps to replace it with alternative rewards. Exercise, creative projects, or meaningful conversations can also trigger positive brain responses.

You do not need to eliminate pleasure from your financial life. You simply want to choose sources of pleasure that do not create long term strain.

When you build alternative coping strategies, spending loses its power as your default response.

Financial Health Begins With Emotional Awareness

Recognizing your emotional spending triggers is not about guilt. It is about clarity. Money decisions are rarely just mathematical. They are emotional.

If you learn to spot the moments when feelings drive your purchases, you gain control. You can decide when spending aligns with your goals and when it is simply a reaction.

Over time, this awareness strengthens both your finances and your emotional resilience. You stop using money as a quick fix and start using it as a tool. And that shift can change everything.